The state of the Pennsylvania gaming industry has never been better.

The Pennsylvania Gaming Control Board (PGCB) unveiled March revenue numbers for the state’s vast gaming market on Wednesday, which includes brick-and-mortar casinos, iGaming, retail and online sports betting, video gaming terminals, and fantasy sports.

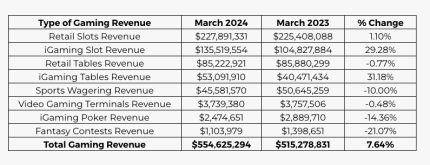

Licensed operators won more than $554.6 million, an all-time monthly record. March 2024 easily bested the state’s previous mark of $534.2 million set in December 2023.

iGaming continued to drive Pennsylvania’s ballooning gaming industry, as all verticals aside from online slots and tables, and a small gain on retail slots, reported year-over-year gross gaming revenue (GGR) declines.

Online slots won $135.5 million, up 29% year over year, while interactive table games won $53.1 million, a 31% improvement from March 2023. Online poker rake added about $2.5 million.

Oddsmakers won almost $45.6 million from bettors last month. The sportsbook revenue represented a 10% decline from the prior year, as March Madness favorites that bettors picked cut into sportsbooks’ bottom lines. The sports gambling income includes bets placed in person and online, though the bulk of the action is made over the internet.

The $554.6 million collective win from all verticals authorized in the commonwealth represented a 7.6% betterment from March 2023.

Pennsylvania’s March gaming win will rank second in the nation behind only Nevada once all of the commercial gaming states disclose their March performances. New Jersey, typically second behind Nevada, this week reported March GGR of $526.6 million.

iGaming continues to flourish in Pennsylvania and in the six other states where online casinos are regulated.

A critical conversation currently occurring in the national gaming industry among stakeholders and lawmakers is determining whether online gambling cannibalizes or complements retail play. In Pennsylvania, the many interactive gaming websites and apps aren’t seemingly helping to grow brick-and-mortar play.

The PGCB March filing shows that Pennsylvania’s 17 physical casinos won about $227.9 million on their slots and $85.2 million on the felt. The combined GGR of approximately $313.1 million represented a trivial 0.6% year-over-year gain.

Parx, the state’s only full-scale casino that’s entirely smoke-free, maintained its market lead with slot and table win of $52.8 million — flat from March 2023.

Wind Creek Bethlehem remained in second with a combined win from slots and tables of $47.7 million. The commercial property owned and operated by the Poarch Band of Creek Indians managed to expand in-person play by more than 6%, or $2.8 million.

A study published this week by Penn State University commissioned by the PGCB and the Pennsylvania Department of Drug and Alcohol Programs found that iGaming participation rose significantly last year. Researchers found that 16% of the adult population in the commonwealth gambled online in 2023, up 5% from 2022.

Pennsylvanians lost more than $2.1 billion in 2023 playing iGaming, iLottery, and betting on sports. Most of the GGR was won on interactive slots and tables — $1.7 billion.

The $2.1 billion in online gambling revenue represented a nearly 27% increase over the preceding year. Pennsylvania, New Jersey, and Michigan have the three richest online gambling markets.

{kind=link}